China sulfuric acid ban hits copper and fertilizer

China sulfuric acid ban is tightening supply for copper leaching and fertilizer makers, raising costs as traders lose a major marginal exporter.

China’s decision to halt sulfuric acid exports from May 1 has turned a specialist chemicals story into a broader commodities warning. By pulling a major marginal seller out of the market, Beijing has tightened supply of an input that sits under copper leaching, phosphate fertilizers and a long list of industrial processes, just as sulfur feedstock had already been squeezed by disruption in the Middle East.

For analysts, the immediate question is not whether sulfuric acid matters. It plainly does. The real question is whether the removal of Chinese cargoes becomes a short, violent squeeze or the start of a more durable repricing across industrial inputs. CRU Group argued that bullish sentiment was already building before the ban, with export quotas cut early in the year and delivered prices into Chile jumping to $270 a tonne from $175 a tonne between late December and mid-April.

But the operator’s problem looks harsher than the analyst’s chart. Acid is not a commodity that can be rerouted or stockpiled without consequence. It is corrosive, regulated and expensive to store. That is why the insider view, from miners to manufacturers, is less about headline prices than about whether enough material can be secured without forcing changes to inventory, shipping and plant design.

Why the market tightened fast

China did not dominate sulfuric acid trade for decades and then vanish overnight. It emerged as a crucial balancing seller because its smelters had surplus material to move, and foreign buyers were willing to absorb it when freight and regulations allowed. Last year that balancing role grew materially. Meena Chauhan, head of sulphur and sulphuric acid research at Argus Consulting Services, told ABC News that China exported close to 5 million tonnes for the first time in 2025, a volume large enough to matter well beyond Asia.

"Last year, they exported close to 5 million tonnes for the first time."

— Meena Chauhan, Argus Consulting Services, via ABC News

CRU’s own estimate was slightly lower at 4.6 million tonnes, but the broader point is the same: China had become the market’s swing supplier. Once Beijing first limited exports through quotas, then moved to an outright halt on May 1, buyers were left scrambling for substitute tonnes in a market that was already tighter than it looked. Scarcity tends to show up first in spot cargoes, then in delivered prices, and only later in production plans.

Viewed through the policy lens, the move looks less like a one-off trade squeeze than a downstream protection measure. ABC’s reporting framed the restriction around fertilizer and domestic industrial needs, while CRU noted that the export halt followed earlier quota controls rather than replacing a liberal trade regime. That sequence matters. Governments usually do not step through quotas, monitoring and then a ban unless they think the domestic opportunity cost of exports has risen.

"It’s a substantial volume in that global trade flow."

— Meena Chauhan, Argus Consulting Services, via ABC News

That helps explain why the policy may prove sticky. If Beijing’s priority is to keep fertilizer inputs and industrial supply chains stable at home, foreign buyers are not competing with Chinese traders alone. They are competing with Chinese domestic policy.

Chile takes the first hit

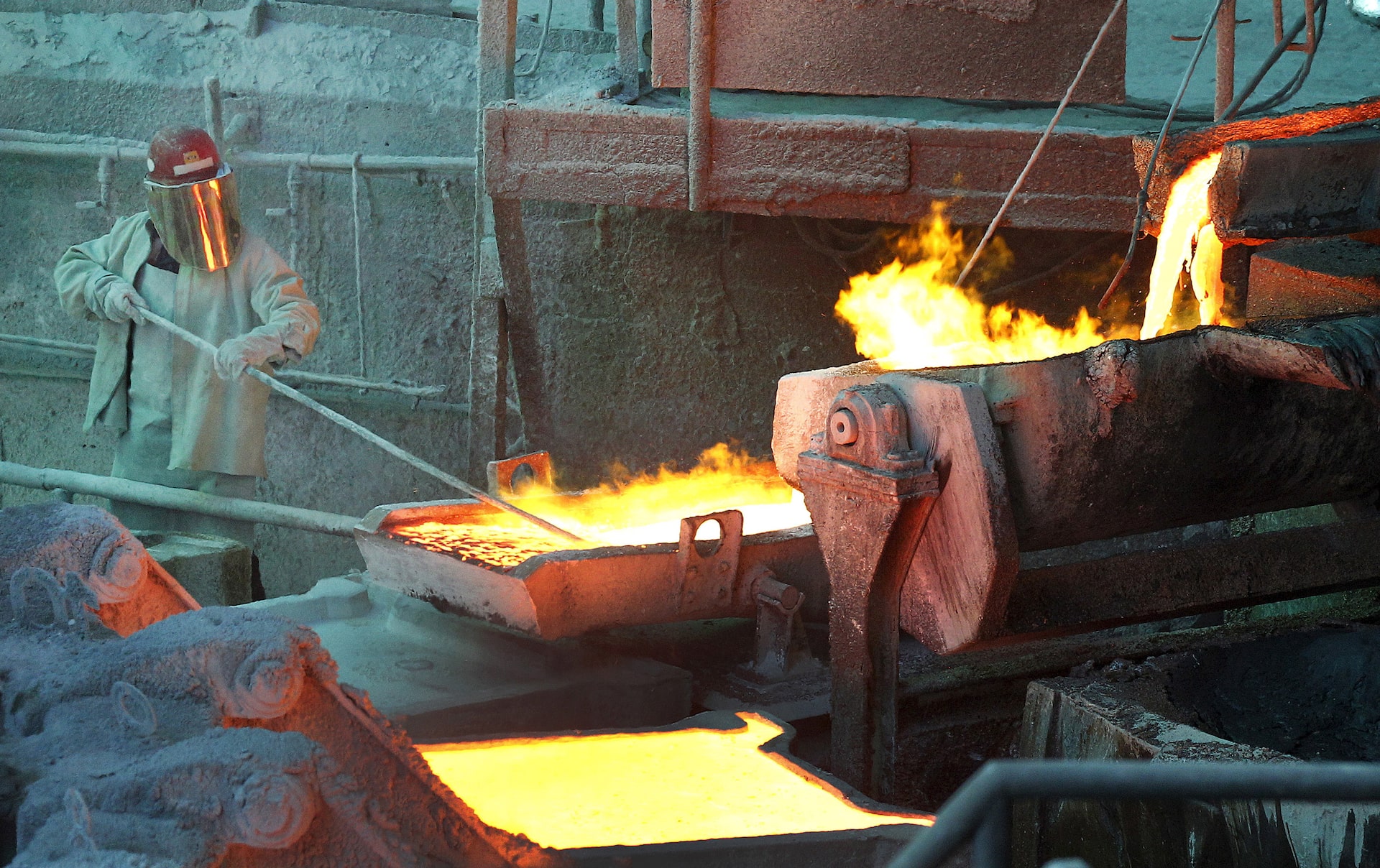

Nowhere is the immediate exposure clearer than Chile. Reuters reported that sulfuric acid is used to produce about half of the country’s refined copper through leaching, which means acid availability feeds directly into mine economics rather than merely nudging them at the margin. For a copper market that was already nervous about supply, that is not a side issue. It is part of the metal’s cost curve.

Plusmining estimated that Chile imported 1.5 million tonnes of sulfuric acid from China in 2025. That does not mean every tonne disappears one-for-one from Chilean consumption this year, but it does show how dependent a key copper producer had become on Chinese surplus. In that sense, the sulfuric acid story looks similar to other commodity pinch points: the market relies on a supplier until that supplier decides the material is more valuable at home.

Costs have already started to reprice accordingly. CRU Group’s analysis said delivered acid prices into Chile rose to $270 a tonne by mid-April from $175 a tonne in late December. Higher prices alone do not shut mines. They do, however, compress margins, alter project sequencing and reward operators with better procurement contracts or captive supply. Andes-focused miners do not need a full physical shortage to feel pain. A market that moves this sharply can force hard choices before tanks are empty.

That is the analyst perspective. The insider perspective is even narrower: how much acid can a buyer physically hold, and for how long? Samantha Van Zyl, chief executive of LoomTex, described the practical limits bluntly in ABC’s report:

"Increasing to the dangerous goods limit actually means that we’re changing the shape of our business."

— Samantha Van Zyl, LoomTex, via ABC News

That line matters because it captures what spreadsheets tend to miss. Sulfuric acid scarcity is not just a price problem. It is a logistics and safety problem. Even when replacement cargoes can be found from Japan, South Korea, Europe or Canada, as ABC and CRU both noted, buyers still have to manage transport times, terminal constraints and storage rules. Not every shortage can be solved with a higher bid.

Why fertilizer and inflation matter too

Copper feels like the cleanest transmission channel because the market is visible and the price discovery is fast. Yet fertilizer may prove the more politically sensitive outlet. Sulfuric acid is central to phosphate processing, which is why Beijing’s decision can be read as an attempt to protect domestic agricultural inputs as much as industrial activity. In a year already shaped by energy and sulfur disruption, that kind of internal prioritization is rational from a policy standpoint, even if it leaves importers exposed.

That is also why the rest of the world should resist reading the ban as a narrow metals story. Bloomberg Markets reported this week that a fertilizer crunch tied to the Iran war was already raising risks for Brazil’s farm economy. The sulfuric acid halt does not create every one of those pressures, but it adds another constraint to the same supply web. Inputs do not have to be identical to reinforce the same inflationary impulse. When sulfur, acid, freight and fertilizer all tighten together, costs start to travel.

From there the regulator-policy perspective comes into focus. Policymakers rarely describe supply-chain pressure in such direct terms. They speak in the language of stability, food security and domestic resilience. Still, the effect is similar. By keeping more sulfuric acid at home, China is forcing foreign buyers to absorb the adjustment through higher procurement costs, longer shipping routes and, in some cases, lower output. For Latin American copper producers and fertilizer users, that looks less like a temporary inconvenience than a reminder that critical inputs can be weaponized quietly.

Scarcity will be rationed by price

Alternative supply exists, and that is the main reason this story is not yet a full-blown industrial emergency. Japan, South Korea, Europe and Canada can all ship sulfuric acid into deficit markets. Chilean miners can renegotiate contracts, alter schedules or accept higher delivered costs. Some downstream users will trim demand rather than chase every cargo. Markets do clear eventually.

But clearing is not the same as healing. When a swing exporter leaves a specialist market, the adjustment usually comes through price first and demand destruction second. That is especially true when the missing volume is measured in millions of tonnes and when the material itself is cumbersome, hazardous and difficult to stockpile. There is no obvious low-friction substitute for a reagent that large parts of the copper and fertilizer chains already depend on.

Put differently, Beijing has not just tightened a chemical market. It has exposed how much of global industry still rests on hard-to-replace inputs that are cheap only until they are scarce. Copper buyers, fertilizer users and anyone still assuming industrial inflation is behind the curve may need to recalibrate around that fact. China’s sulfuric acid ban is not the biggest commodities shock of 2026. It may, however, be one of the clearest examples of how strategic supply power now works: quietly, upstream and with the bill arriving later.

Reza Najjar

Commodities desk covering oil, natural gas, gold and base metals. Reports from London.