Custody bank stocks beat in Q1 as flows stay uneven

Custody bank stocks beat estimates in Q1 as Ameriprise and Franklin turned bigger asset bases and fee income into stronger earnings.

Custody-bank and wealth-management stocks came through the first-quarter reporting season with a simpler message than the market noise around them: bigger fee-bearing asset bases are still overpowering patchier client flows. Ameriprise Financial and Franklin Resources both delivered quarters that were strong enough to keep investors focused on revenue quality rather than on every swing in sentiment, suggesting this part of finance can still earn through volatility so long as advisers keep assets sticky and product mix keeps improving.

An IndexBox sector screen put aggregate revenue for the group 2.9 per cent above expectations. Ameriprise reported first-quarter revenue of $4.77bn, up 10.8 per cent from a year earlier, while Reuters reported that Franklin’s fiscal second-quarter revenue rose 8.7 per cent to $2.29bn. The sector-level read is useful because it shows where investors are drawing the line: a firm does not need immaculate flows to win credit for the quarter, but it does need a fee base large enough to absorb the noise.

But the same quarter looks different depending on where one sits. From inside the firms, the story is about whether bigger advisory networks, bank partnerships and broader platforms can keep monetising client assets even when flows wobble. From the analyst seat, the sharper question is whether Franklin’s gains are coming from higher-fee products quickly enough to change the earnings mix. From the skeptical angle, the quarter may be benefiting from the very backdrop that could complicate the next one if long-dated Treasury yields keep testing highs and volatility keeps clients cautious.

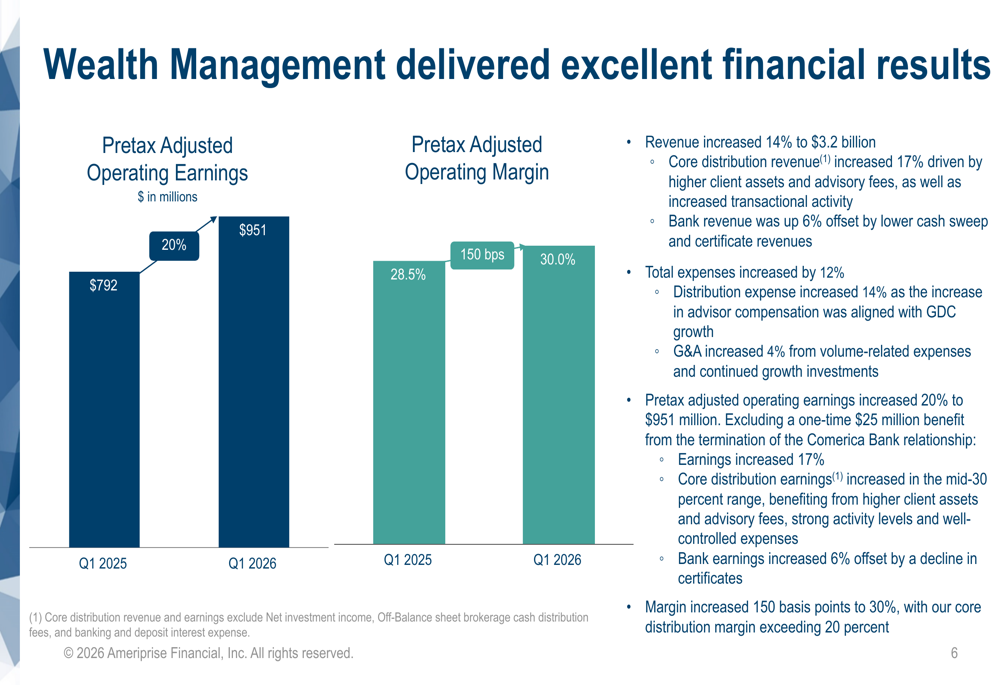

Inside Ameriprise, that case was explicit. In its first-quarter release, chairman and chief executive Jim Cracchiolo argued the model is still doing exactly what management built it to do: throw off advice, wealth and asset-management revenue at the same time.

Ameriprise delivered a strong start to the year, with significant revenue and earnings growth driven by the durability of our business and consistent execution of our strategy.

— Jim Cracchiolo, Ameriprise Financial

Beneath that statement sits the more important detail. Reuters reported in January that client assets reached a record $1.7tn, and the later quarter showed why that scale matters. Even with adviser departures tied to the Comerica transition and tougher recruiting competition, WealthManagement reported that Ameriprise cut net outflows. That suggests existing adviser productivity and the Huntington Bank pipeline are doing at least part of the work that pure recruiting once had to do. Not a perfect flows story. A sturdier fee-engine story.

Assets over flows

For this group, that distinction matters because custody-bank and wealth-manager names are often judged as if one quarterly flow line settles the whole argument. Q1 suggested the opposite. When assets under management and administration are already large, even a messy market can still generate more advice fees, platform revenue and administrative income than investors expected. The beat, in other words, was less about heroic asset gathering and more about how large installed balances keep earning when the quarter gets uncomfortable.

Macro conditions helped, even if they did not help cleanly. Bloomberg reported that the 30-year Treasury yield touched its highest level since 2007, while CNBC reported that foreign government selling and currency worries were adding to bond-market strain. Elevated yields can pressure risk appetite and complicate fixed-income marks. They can also raise returns on cash and short-duration allocations that stay inside wealth platforms. For firms paid on advice relationships, allocation shifts and administration, that is a meaningful offset.

At Franklin, the analyst version of the story came through more clearly. Reuters said revenue rose to $2.29bn on stronger inflows and fee income, and the company’s SEC-filed earnings release said it generated $17bn in long-term net inflows across public and private markets. The issue for Franklin has not been whether it can produce a better quarter on paper. It has been whether the better quarter is being driven by businesses that deserve a better multiple.

Franklin Templeton delivered another strong quarter, with $17 billion in long-term net inflows across public and private markets, reflecting the strength of our diversified global platform.

— Jenny Johnson, Franklin Resources

Taken together, the signals point to a partial yes. Franklin highlighted inflows across public and private markets rather than leaning on a single legacy franchise, and the strategic backdrop in the fact pattern points to a firmer push into alternatives, ETFs and customised indexing through Canvas. That goes directly to the analyst concern about mix. If more of the uplift is coming from products clients are actively choosing, rather than simply inheriting through market appreciation, the revenue line looks more durable and the quarter reads as more than a temporary lift from better market levels.

Scale and product mix

Viewed strategically, this corner of finance is beginning to trade less like a simple market beta story and more like a distribution-and-product-mix story. Scale still matters. By itself, though, scale is no longer the moat. The moat is the ability to route clients through advice channels, bank partnerships, private assets, ETFs and custom strategies that keep fee capture intact when public markets become choppier.

Seen that way, Ameriprise’s Huntington distribution partnership and Franklin’s platform broadening point in the same direction. The likely winners are not necessarily the firms with the cleanest quarter-end flow print. They are the firms with enough channels to keep assets inside the system and enough product breadth to keep charging for them. That is why Ameriprise could post a strong quarter while still working through adviser attrition, and why Franklin’s inflow story looks better when it is paired with higher-fee businesses rather than judged as a standalone volume number.

Yet the skeptic’s question has not gone away. If long-end yields remain elevated and volatility keeps clients defensive, firms across the sector may discover that sticky fee revenue can cushion demand weakness only for so long. Clients can hold more cash, delay reallocations and become more selective about risk. That helps some platform revenues in the short run, but it is not the same thing as broad-based appetite returning to active products, alternatives or fresh advice mandates.

So the strong quarter should probably be read as a quality-of-revenue signal rather than as an all-clear on flows. Ameriprise and Franklin showed that larger asset bases, wider distribution and better mix can still produce earnings momentum in an awkward rates backdrop. The next test is whether that formula keeps working when volatility stops flattering the fee base and the easy comparisons get harder. For now, custody-bank and wealth-manager stocks are being rewarded not because the market looks calm, but because their fee engines still do not require calm to deliver.

Sloane Carrington

Markets columnist. Analytical pieces and deep-dives on monetary policy, capital flows and corporate strategy. Reports from New York.