Nvidia and retail earnings will test the AI rally's limits

This week's Nvidia and retail earnings will show whether AI spending can keep carrying stocks as inflation and renewed Fed fears start to hit consumers.

After an 18 per cent rise in the S&P 500 since the March low and a 36 per cent jump in Nvidia over the same stretch, Wall Street heads into this week’s results with a simple question. Can one company still do most of the lifting for equities that have grown comfortable ignoring hotter inflation, or will a run of retailer reports show that tighter money is finally catching the household that underwrites the rest of the index?

Nvidia and a cluster of consumer names belong in the same frame. One side of the earnings calendar tests whether the AI capital-spending cycle can keep expanding fast enough to defend one of the richest valuations in the index. The other tests whether shoppers, after April retail sales rose 0.5 per cent — a number helped by higher prices and tax refunds, not just stronger volume, are still spending with the same ease implied by share prices that show no sign of a consumer pullback.

The S&P 500’s 18 per cent climb since March looks broad at a glance. But the speed of the semiconductor move and Nvidia’s own rebound means money has kept returning to one familiar refuge: revenue streams seen as less exposed to the household and less sensitive to the next turn in policy. The pricier that refuge gets, the more stocks need corroboration from somewhere else.

Allen Bond of Jensen Investment Management put the first question plainly in remarks reported by Reuters: “What we need to see from Nvidia is evidence that justifies the increase in the stock price and justifies their position and their benefit from this increased spending in data centers.” Equities have rewarded the company as if the answer is already yes. Proving that AI demand is still widening — not merely holding — is the harder part.

The macro backdrop now is tougher than a month ago. CNBC, citing CME FedWatch positioning after the latest inflation surprise, said traders were assigning a 51 per cent probability to a December Federal Reserve rate increase. If rates stay higher for longer, the discount rate on long-duration growth stories rises just as households face steeper borrowing costs, more expensive fuel and tighter room for discretionary purchases.

The narrow market problem

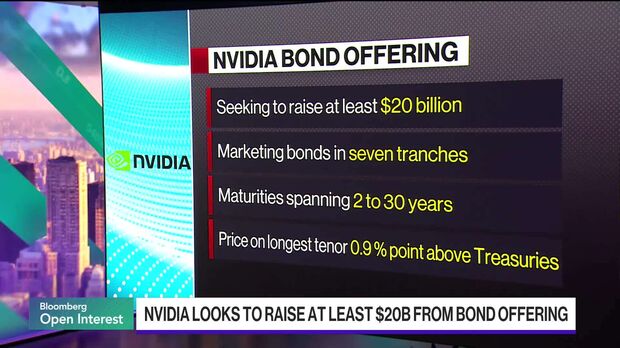

Nvidia’s role in the argument is outsized because the stock has become both a company and a market shorthand. Reuters said the shares are up 36 per cent since the March low, while the Philadelphia SE semiconductor index has rallied 60 per cent this year. With leadership looking like that, the issue is not only whether Nvidia beats. It is whether management can still describe a demand curve that stretches past the current build-out cycle, especially after investors looked past strong results in February and focused on returns from all that spending.

Yung-Yu Ma of PNC Financial Services Group, again speaking in Reuters’ week-ahead report, argued that the more immediate test is whether Nvidia can “defend its leadership position” the way it has over the past few years. The question is no longer whether AI is real. It is whether equities can keep paying a premium multiple for the same leader once competition, procurement discipline and sheer base effects become part of the story.

An earnings beat by itself may not settle that. The Street will want to hear whether spending from cloud groups and enterprise buyers still looks urgent rather than front-loaded, and whether customers are treating new GPU capacity as necessary infrastructure instead of a race that peaks too early. If executives sound confident but less expansive, the stock becomes a valuation argument rather than a growth one — and narrow rallies tend to wobble at that point.

The consumer check

Retailers matter for a different reason. The S&P 500 can absorb a concentrated tech rally for only so long if the consumer complex starts describing trade-down behaviour, thinner baskets or heavier promotion. Reuters’ April retail sales report showed a 0.5 per cent increase, but the same story noted that higher prices helped lift the total and that inflation was starting to press on demand. For anyone holding the broad tape, that is less reassuring than a clean volume-led spending gain would have been.

Retail commentary, not just the sales print, cuts closer to the broad-market story. Ma told Reuters that “what is more at stake for the retail earnings is, how resilient is the consumer?” Retailers do not need to report a collapse to unsettle positioning. They only need to show that middle-income shoppers are becoming selective while input costs and wage bills remain sticky. Margin pressure can do the rest.

Walmart sits near the centre of that question. In February, Reuters reported that Walmart’s new chief executive began his tenure with a cautious outlook despite another quarter of steady sales. That was before the latest inflation jolt reshaped rate expectations.

If similarly defensive language now spreads across big-box and discretionary names, equities will have to confront the possibility that resilient spending was partly a timing story — helped by refunds and still-solid employment — rather than proof that consumers can shrug off tighter conditions indefinitely.

Stronger inflation pushes bond yields up. Higher yields tighten financial conditions. Tighter conditions eventually reach households through credit cards, auto loans and confidence, even if the first few retail sales reports hold together. This week looks less like a routine earnings batch and more like a stress test for two assumptions that have coexisted without much friction: that AI capex remains insulated from the cycle, and that the US consumer remains sturdy enough to keep the rest of corporate America out of trouble.

Should both assumptions hold, equities keep their current shape — Nvidia continues carrying the narrative at the top of the index, and retailers reassure investors that the underlying demand base has not cracked. If one breaks, the interpretation changes fast. A softer Nvidia outlook would raise fresh questions about how much of the rally rests on one capital-spending theme. A cautious read from retailers would suggest that rate pressure is reaching Main Street sooner than the headline indices imply.

No single release will give a neat answer by Friday. Investors should still get something more useful: a read on whether the market’s favourite growth story and its broadest spending base are moving in the same direction. In a year when policy fears have returned and the S&P 500 has still climbed 18 per cent from its March low, that alignment matters more than another routine beat or miss.

Sloane Carrington

Markets columnist. Analytical pieces and deep-dives on monetary policy, capital flows and corporate strategy. Reports from New York.