Nvidia’s $25 billion bond sale shows AI’s cash king joining the borrowing spree

Nvidia raised $25bn in June, upsized from an initial $20bn, as investors piled in — a sign the AI winners are financing expansion with debt not just cash.

Nvidia’s $25 billion bond sale is a sign that the biggest winners in artificial intelligence are starting to finance expansion the old-fashioned way: by tapping credit markets.

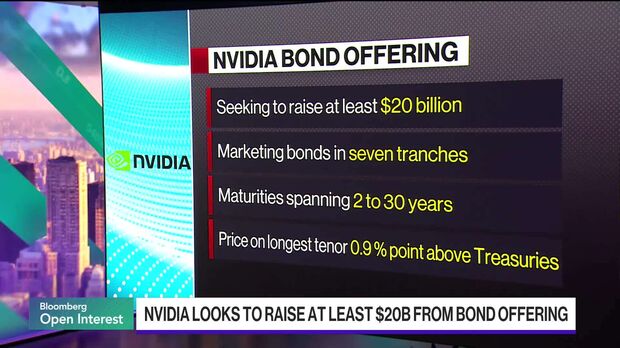

Nvidia (NVDA) offered notes across seven maturities in mid-June 2026, initially targeting roughly $20bn before the deal was upsized to $25bn after about $85bn of investor demand, according to Bloomberg. The company sold tranches from two-year paper out to 30-year debt as banks including JPMorgan, Goldman Sachs and Morgan Stanley led the books. Bloomberg’s market report said orders were ‘massive’, and CNBC’s coverage confirmed the upsizing and the syndicate’s role in marketing the deal. CNBC reported that proceeds will give treasury optionality for capex and potential strategic investments without diluting equity.

What the numbers show

Headline figures are clear: $25bn raised, $85bn of demand, and maturities stretching to 30 years. That scale puts Nvidia among the largest corporate borrowers of the year and underscores investor confidence in a company that still sits on a large cash position but is choosing to borrow. The Financial Times framed the move as part of a broader wave of tech issuance testing investor appetite for long-dated technology credits. The FT’s analysis argued the sale signals a structural shift: equity-rich tech firms are now comfortable layering in leverage to fund the next phase of AI infrastructure.

Why finance, not equity?

Nvidia chose to tap the bond market despite strong free cash flow for several reasons. Low borrowing costs relative to the return on AI projects make debt an efficient tool: issuing long-term bonds locks in financing at fixed rates while preserving ownership. Credit desks point to tightened spreads in the high-grade market for top-tier issuers, and analysts say the $85bn book allowed the company to price the deal attractively. Some market participants also said the timing — after several large tech deals — made Nvidia’s name notably liquid for buyers.

“I’m not surprised they would do a drive-by,” CreditSights analyst Andy Li told Bloomberg, capturing the sense that investors will buy top-tier AI names even when issuance volumes surge. The demand pool for the best-rated tech credits has widened as yield-seeking global funds hunt duration and quality.

How this changes the capital cycle

For years, big tech hoarded cash and leaned on equity financing when needed. The turn to large-scale debt suggests the next phase of the AI investment cycle will be financed through a mix of cash, targeted M&A, and bond issuance. That matters for corporate strategy and market structure: borrowing reduces near-term equity dilution, but it increases fixed obligations and the sensitivity of outcomes to an economic slowdown.

One immediate implication is on cost-of-capital math. If Nvidia can push spreads tight on multiple maturities, the weighted-average cost of its new capital could be lower than issuing equity to fund multi-year data-centre and chip fabs — a trade-off CFOs prefer when they expect high, reliable returns on incremental investment.

Market plumbing and crowding risk

The surge in tech issuance raises the question of market capacity. A single $25bn deal consumes a meaningful share of the high-grade new-issue calendar. If several large issuers follow suit, investor appetite could be tested, particularly in long maturities where pension funds and insurers supply demand but are sensitive to duration and regulatory considerations.

The FT noted that an expanding pipeline of tech debt could widen the required pool of long-duration buyers. That, in turn, may to compress secondary liquidity for lesser-known issuers and push yields wider for mid-tier credits when supply outpaces demand.

What the treasury playbook looks like

From a treasury perspective, debt issuance yields optionality. The proceeds can refinance existing maturities, fund capital expenditure, or be held as dry powder for acquisitions or partner investments. Corporate treasuries value the predictability of fixed-rate long debt when planning multi-year capex for data centres and fab expansions.

For Nvidia specifically, the mix of maturities implies a dual strategy: short paper gives flexibility; long paper locks in long-term funding for multi-decade assets. The company’s strong market position and franchise pricing power make that feasible.

Forward look

The $25bn deal is both a symbol and a practical accelerator. It signals that even the market’s richest AI winners see debt as a viable lever, and it gives competitors a blueprint for financing large-scale infrastructure without immediate equity issuance. That could accelerate the pace of data-centre buildouts, partnerships, and hardware contracts — a boon for suppliers but a circular pressure on capital markets.

The near-term risk is twofold: compression in demand if multiple large deals come at once, and credit-market sensitivity to a macro shock that reprices long-duration corporate debt. Monitoring secondary-market spread moves on Nvidia’s new paper will be an early test — if yields stay tight, the market has ample room; if they wobble, the crowding story fast becomes a liquidity story.

—

“I’m not surprised they would do a drive-by,” — Andy Li, CreditSights, on investor appetite for top-tier AI borrowers. Bloomberg link

Avery Lin

Markets editor covering US equities, single-name stocks and quarterly earnings. Reports from New York.